Introduction

Oil prices are back at their pre-conflict levels, as core Inflation puts in another high. The original framing, where energy prices were completely driving the inflation data, is wrong, as even energy-corrected inflation is up to 3.4%, strengthening the rate hike case, creating risk-off pressure.

Global Macro

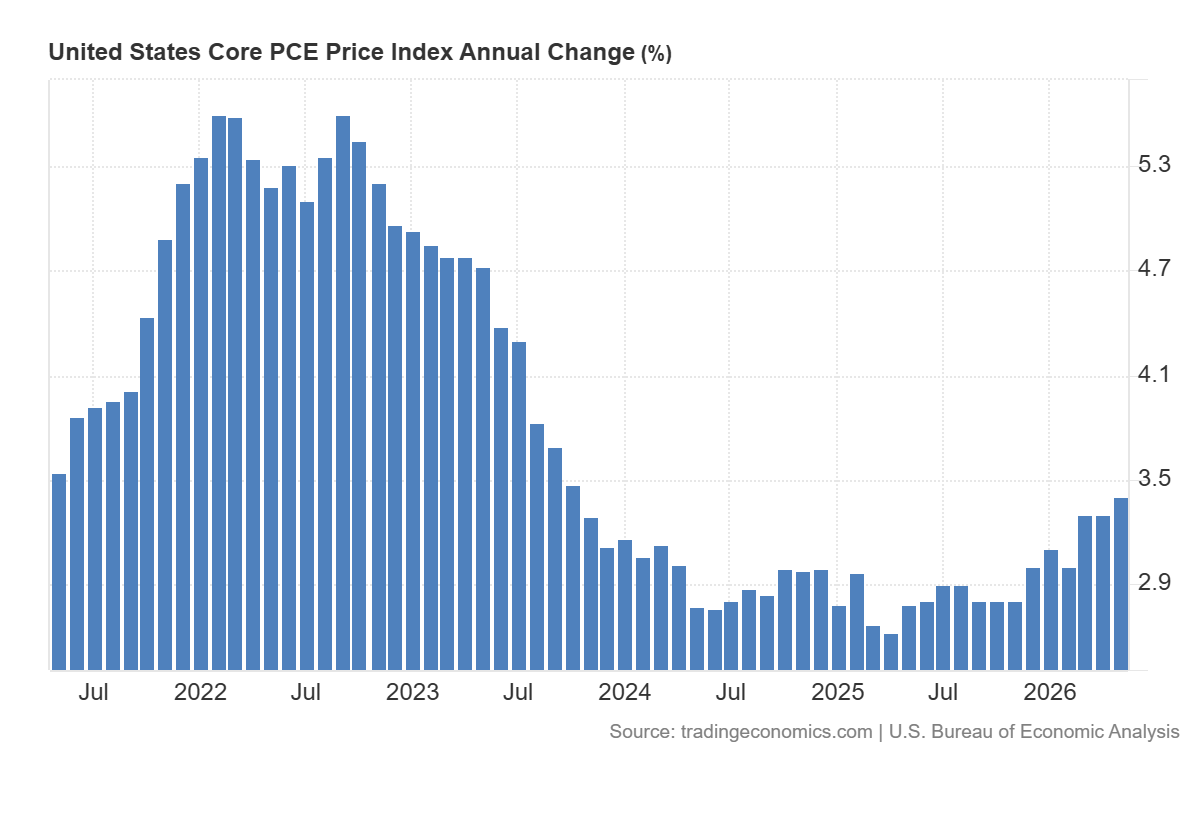

This week’s headline event was the core PCE Index, which came in at 3.4% year-on-year.

With oil prices back in the low 70s, the trigger that originally caused the rate hike debate has disappeared. However, this week’s core PCE shows that there is more going on than just energy prices. The core index, which includes this measure, still gave a 3.4% reading, which is far over the 2% target. But more importantly, it shows that inflation since the start of 2025 has been trending up. This data thus maintains the possibility of a rate hike later this year.

Equities

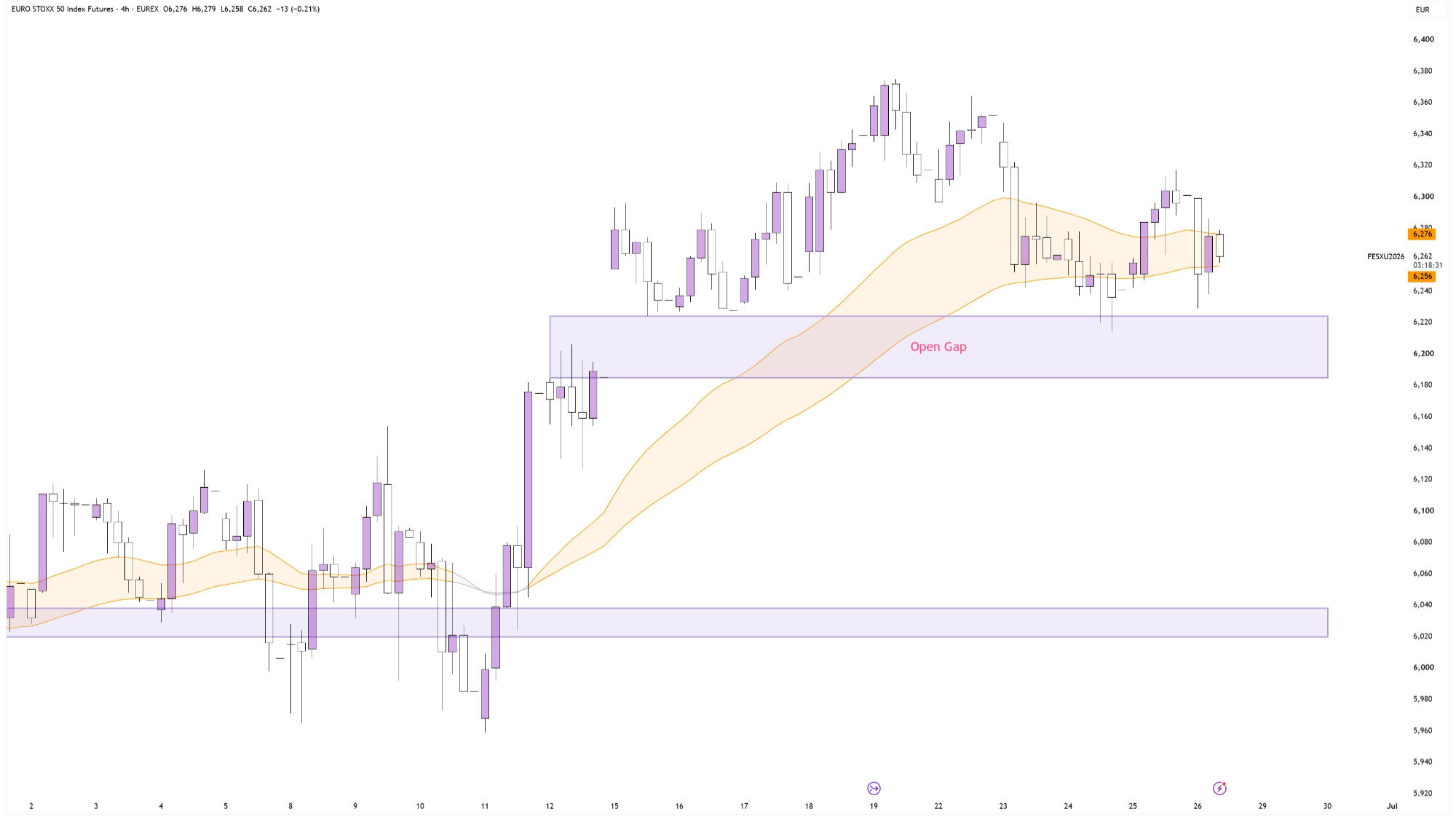

All across the board, stocks had a much-needed breather at their ATHs. Comparatively, the Euro Stoxx put up the best week of all.

Euro Stoxx 50 on the 4-hour Timeframe

Due to this strong week, it managed to react from the open gap, rather than filling it, which all other indices did this week.

Forex

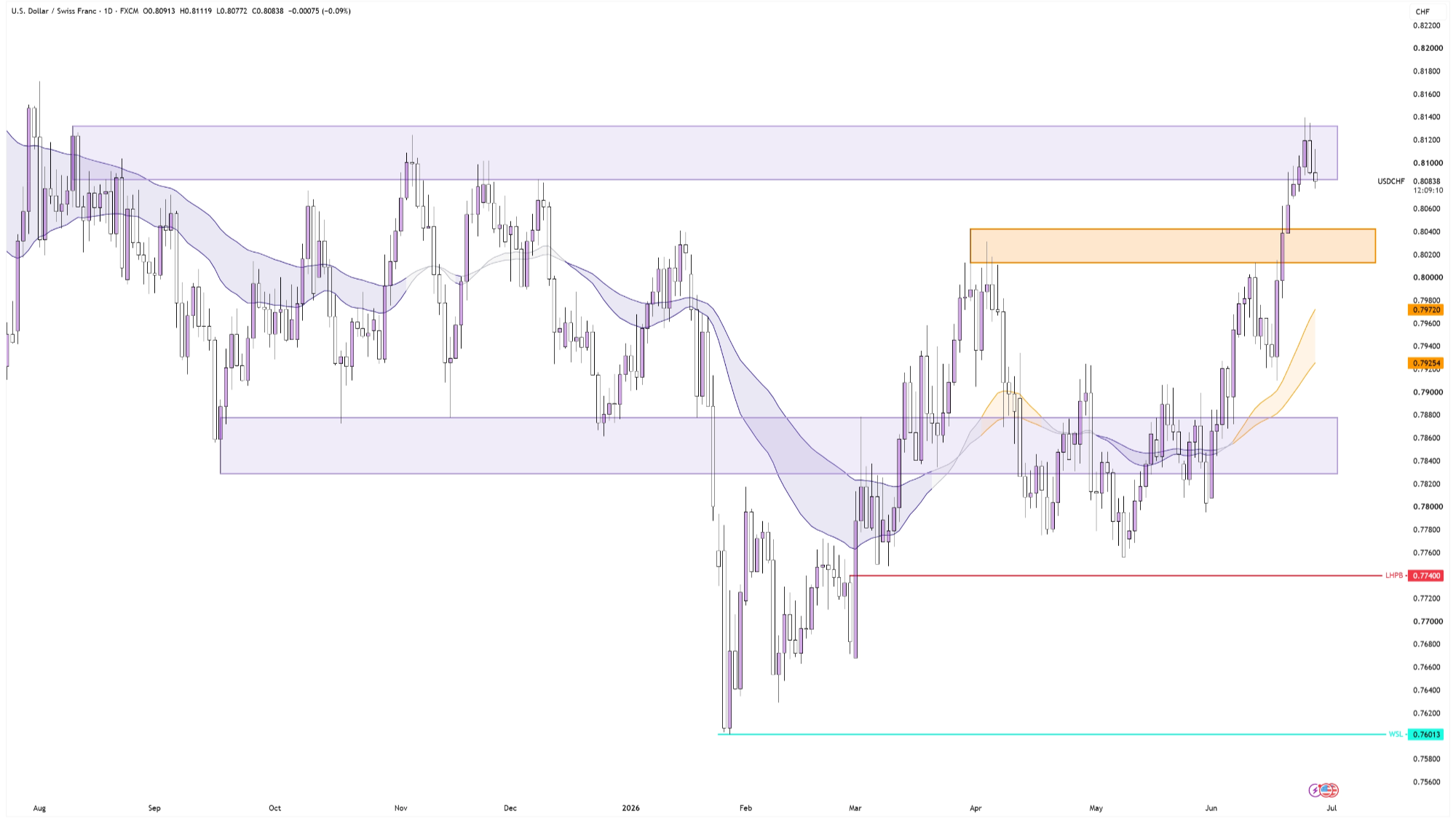

The US Dollar has been recovering from 15-year lows against the Swiss Franc, driven by rate hike expectations, while the SNB is expected to hold rates for the foreseeable future. This has put the pair back in a former, exceptionally clearly defined range.

USD/CHF on the Daily Timeframe

Technically, this chart looks like it wants to break out from this former range, especially as the 0.801–0.804 range provides an exceptional amount of support. However, because we are on the daily timeframe, fundamentals come into play, and a big part of what decides how this will resolve is key inflation data for both the US and Switzerland.

Commodities

In last week’s market pulse, we outlined a specific path for oil to take, stating that the oil inventory and trade rebuild would take some time, likely meaning that the asset doesn’t go quite back to its pre-conflict levels just yet.

Oil on the Daily timeframe

However, the asset dropped further than expected and is now touching the open gap. That doesn’t invalidate the original reasoning, but it does mean we have to adjust our expectations to something resembling the above scenario, where a close of the open gap provides support and may cause a small bounce.

Conclusion

One-sentence summary of the week:

Even Without Oil, Inflation is High. What Will Central Banks Do About It?