Introduction

This week was defined by a flurry of interest rate decisions, as all seven major central banks decided on their interest rates. While policymakers dominated the headlines, equities continued to struggle, and oil prices shot upward, creating a complex mix of second-order effects.

Global Macro

With seven major central bank meetings in a single week, there is plenty to unpack. While we can’t dive into every line of the transcripts, here is a high-level summary of the key takeaways.

- U.S. Fed: Held rates as expected, but future guidance was rather hawkish. There are now zero-rate cuts priced in. However, Powell clearly noted that there’s a lot of uncertainty due to the conflict in the Middle East, and that the resolution or continuation of this conflict will have a big impact.

- EU ECB: The ECB also held steady. With inflation sitting at 1.9%, the bar for further movement is high, though officials noted potential energy-driven price spikes as a threat.

- Rates held constant at 0.75%, but the narrative is shifting. Markets now anticipate further increases, potentially arriving sooner than the initial consensus suggested.

- Australian RBA: Hiked rates by 25 bps, as inflation has been consistently above target for over a year now. Notably, however, this decision was only passed with a 5-4 vote, indicating a likely pause at the next meeting

- Canadian BoC: Held rates steady but highlighted a growing dilemma. The Canadian economy is showing signs of exhaustion, yet the threat of resurgent inflation may eventually force the bank to prioritize one side of its dual mandate over the other.

- British BoE: As widely expected, rates were kept stable, but the tone was much more hawkish than originally expected. Rate hikes are now openly being discussed.

Equities

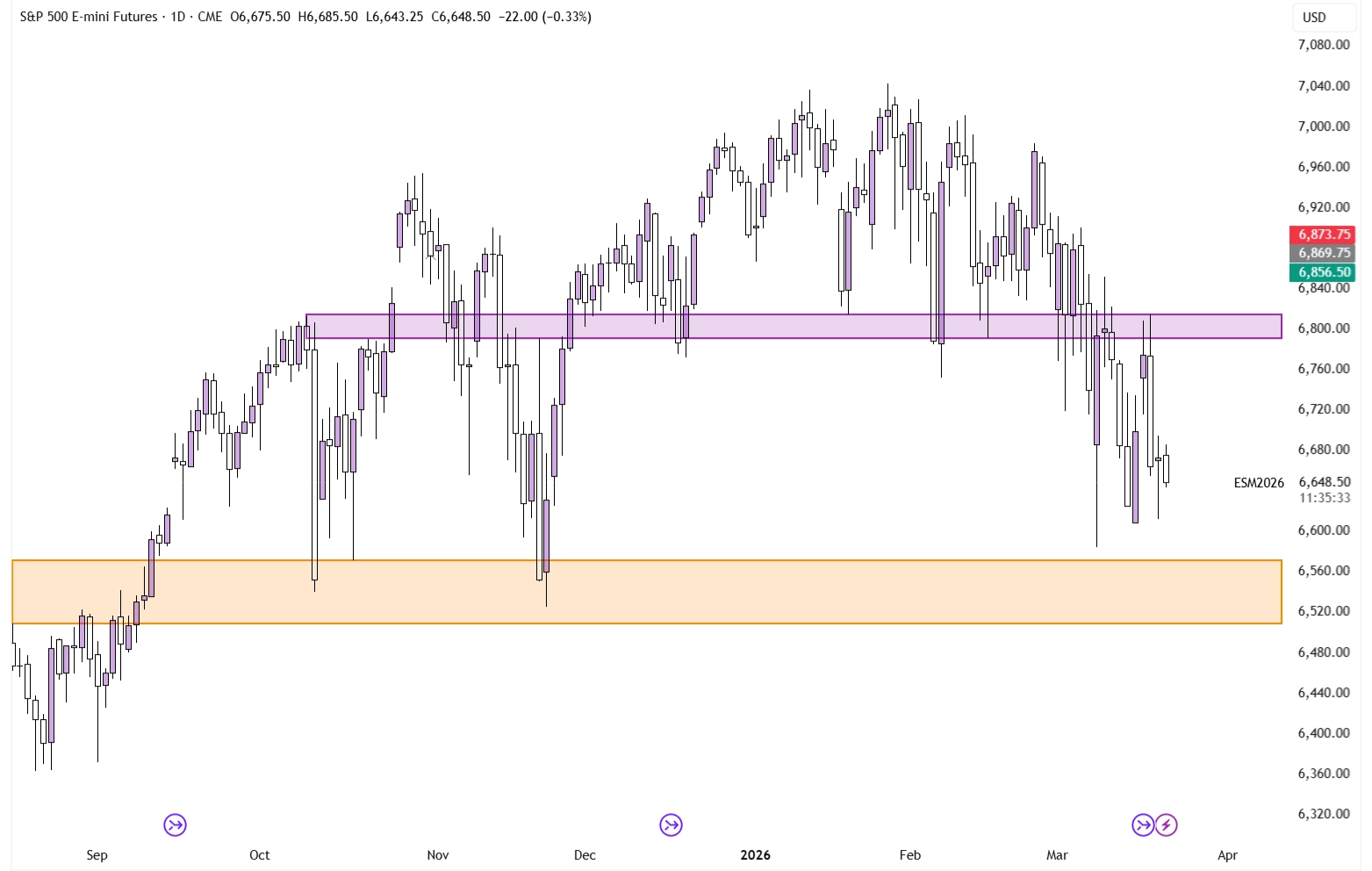

It was a difficult week for the indices, with major benchmarks ending the session in the red. The S&P 500 attempted an early-week rally but stalled precisely at a key Resistance level.

S&P 500 on the Daily Timeframe

With that rejection, the attention shifts to the downside, where we find an equally important Support zone at $6,508-6,571. At this point, the market seems stuck between those two levels and seems set for a test of the support zone, with the current triple low appearing rather weak, due to its lack of excess.

Forex

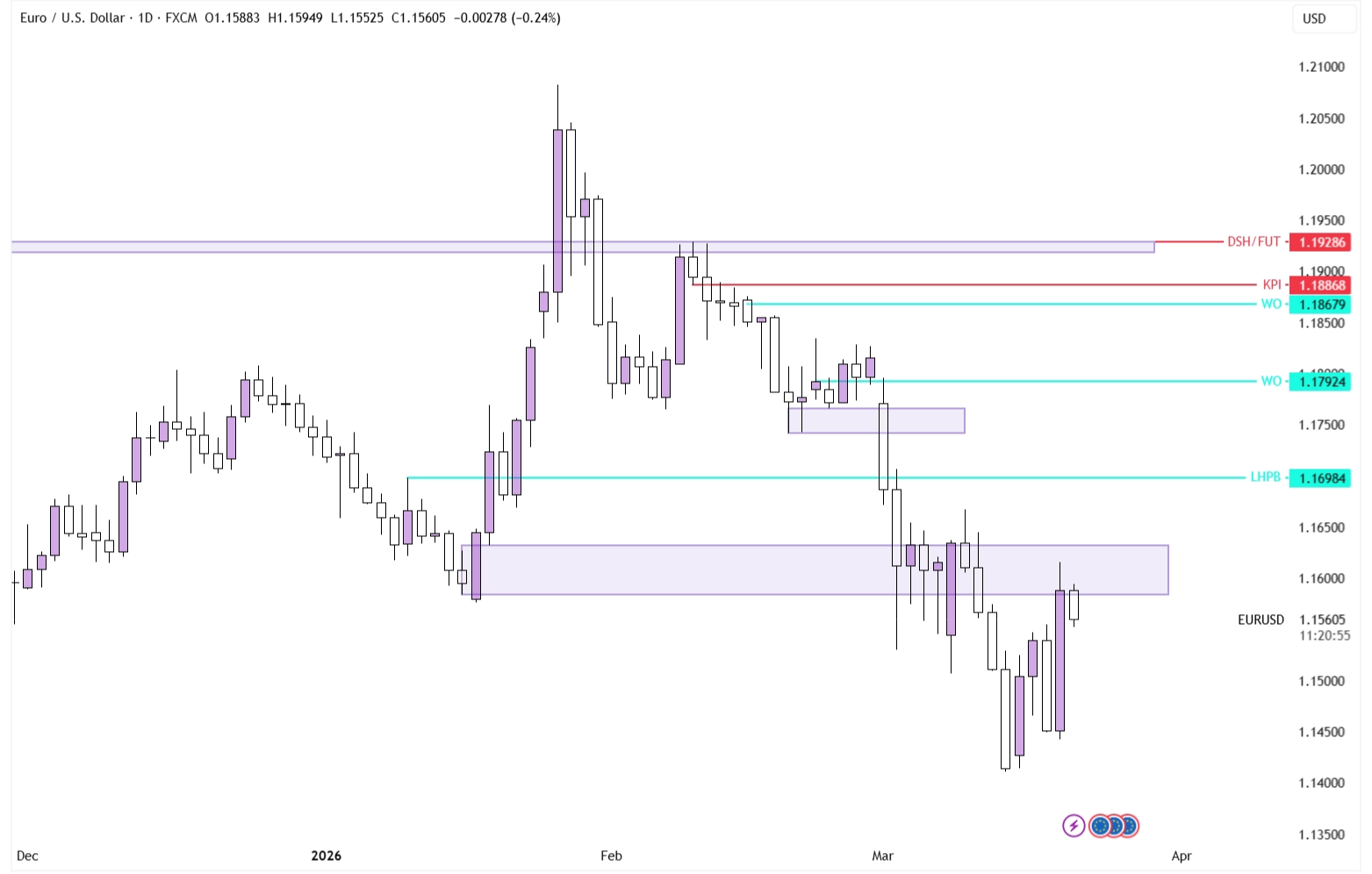

The combination of both the ECB Interest Rate decision, as well as the FOMC, gave a week of interesting price action in EUR/USD. On Wednesday, the pair closed decisively lower as the Fed’s hawkish stance strengthened the Dollar (higher relative rates drive currency strength).

EUR/USD on the Daily Timeframe

However, Wednesday’s price action was completely engulfed with a true bullish engulfing on Thursday, as the ECB, in its turn, also sounded hawkish. Despite not giving much info away, the markets interpreted the meeting as strong for the Euro, pushing prices up right into this key area of old lows.

From a technical perspective, the picture is a bit muddy. We see conflicting signals: the bullish engulfing candle suggests upward momentum, yet the price is stalling right at a known Resistance zone.

In situations like this, it’s often wise to just stand aside and wait for the market to tip its hand according to where it wants to go. If price manages to break through the resistance level, then this chart will look bullish, warranting longs. On the other side, however, any bearish price action at the current level would confirm that the bottom at 1.141 is vulnerable.

Commodities

Despite the ongoing geopolitical friction in the Middle East, Oil remained relatively contained this week. Prices fluctuated within a $10 range (narrow by recent standards) and look set to close the week as an Inside Week.

Oil on the Daily Timeframe

Conclusion

One-sentence summary of the week:

Higher Oil Prices and Weakening Stocks Force Central Banks into a Defensive Position