Introduction

Markets calmed down for a bit as the economic calendar slimmed down for this week, and the Iran - U.S. war seems to have reached a breather. However, next week is set to provide us with a completely action-packed calendar, along with a possible end to the ceasefire.

Global Macro

A relatively light economic schedule saw most focus on Canadian CPI, which came in lower than expected. As we’ve discussed before, current inflation data is a bit tricky as it doesn’t reflect the rise in energy prices yet, which we know is coming and is thus seen as less reliable by markets.

However, that doesn’t mean that markets are completely overlooking any current data. In fact, because CPI came in at 2.3% year-over-year, lower than the 2.4% consensus, it means that the BoC will have a bit more of a buffer to absorb the upcoming uptick in inflation as initially thought.

Equities

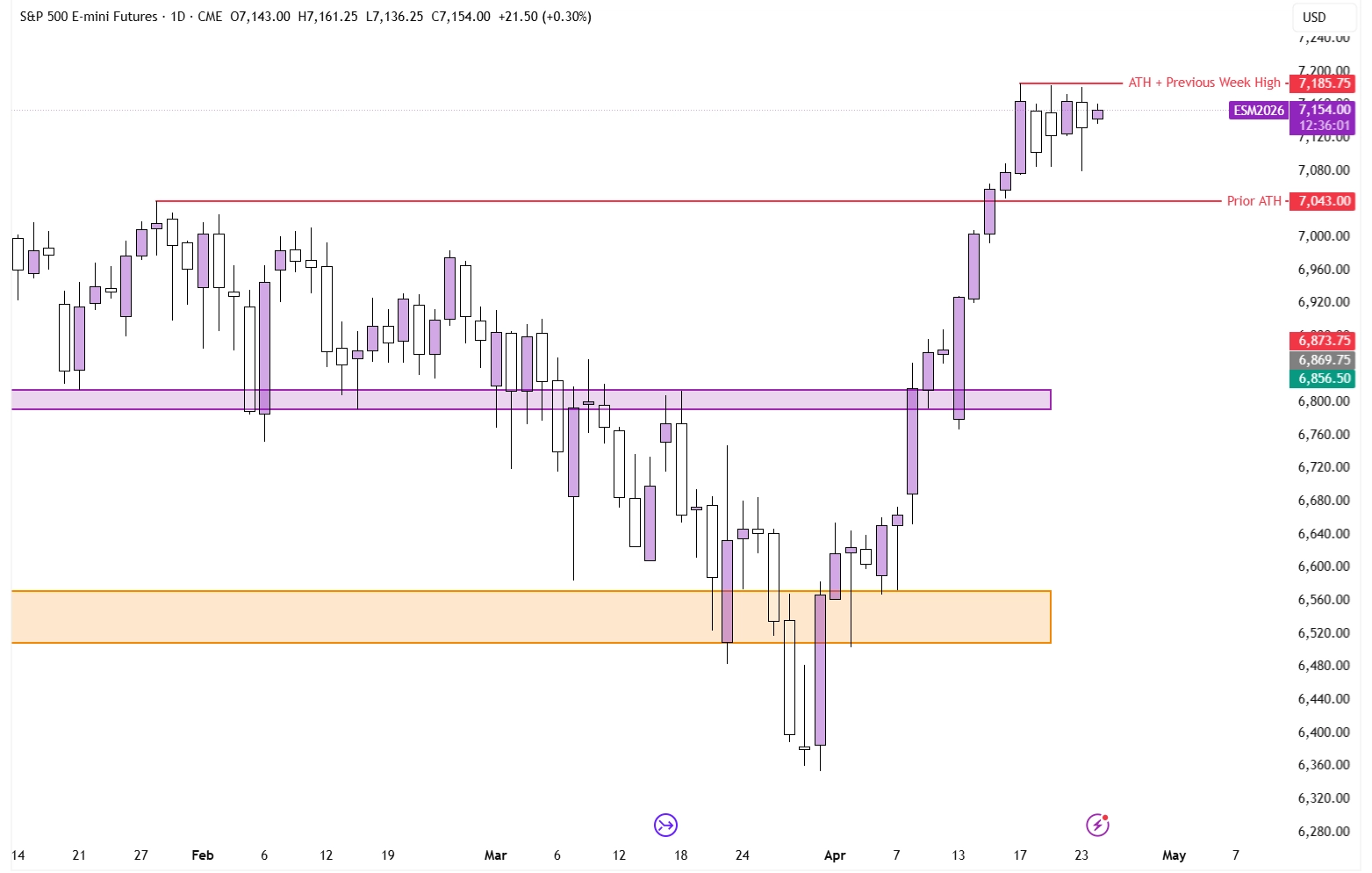

Off the back of the stellar week we had earlier, stock prices decided to take a breather this time around. The S&P 500, for example, is set to close as an inside week (this week’s high and low are contained entirely within last week’s extreme points).

S&P 500 on the Daily Timeframe

While an Inside Bar is not a directional candlestick pattern, but rather one that shows price compression, we could interpret it as a bullish factor in this context. Technically, the current trend is very clearly up, and with how strong the past two weeks were, some consolidation should help to sustain its recent momentum.

However, that doesn’t mean we won’t see a small probe below this week’s low. In fact, inside bar patterns are quite prone to testing liquidity on one side of the candle, before then reversing to the opposite side. A bullish setup coming into next week could thus look something like the following:

S&P 500 on the Hourly Timeframe

While a bullish argument can be made when looking at charts, all of this is very reliant on the fundamental factors that are driving prices right now. There’s a lot of uncertainty in financial markets, on the one hand in the form of the U.S. - Iran conflict, where the current ceasefire appears to be somewhat fragile.

On the other hand, Jerome Powell will soon step down as Fed chair, with Kevin Warsh taking his place. Because he was nominated by President Trump, some investors are wary of potential political influence on monetary policy, alongside the general unknowns that come with any new Fed Chair’s established policy stance.

Both of these factors are big risks, and any breaking or unexpected news could quickly invalidate setups.

Forex

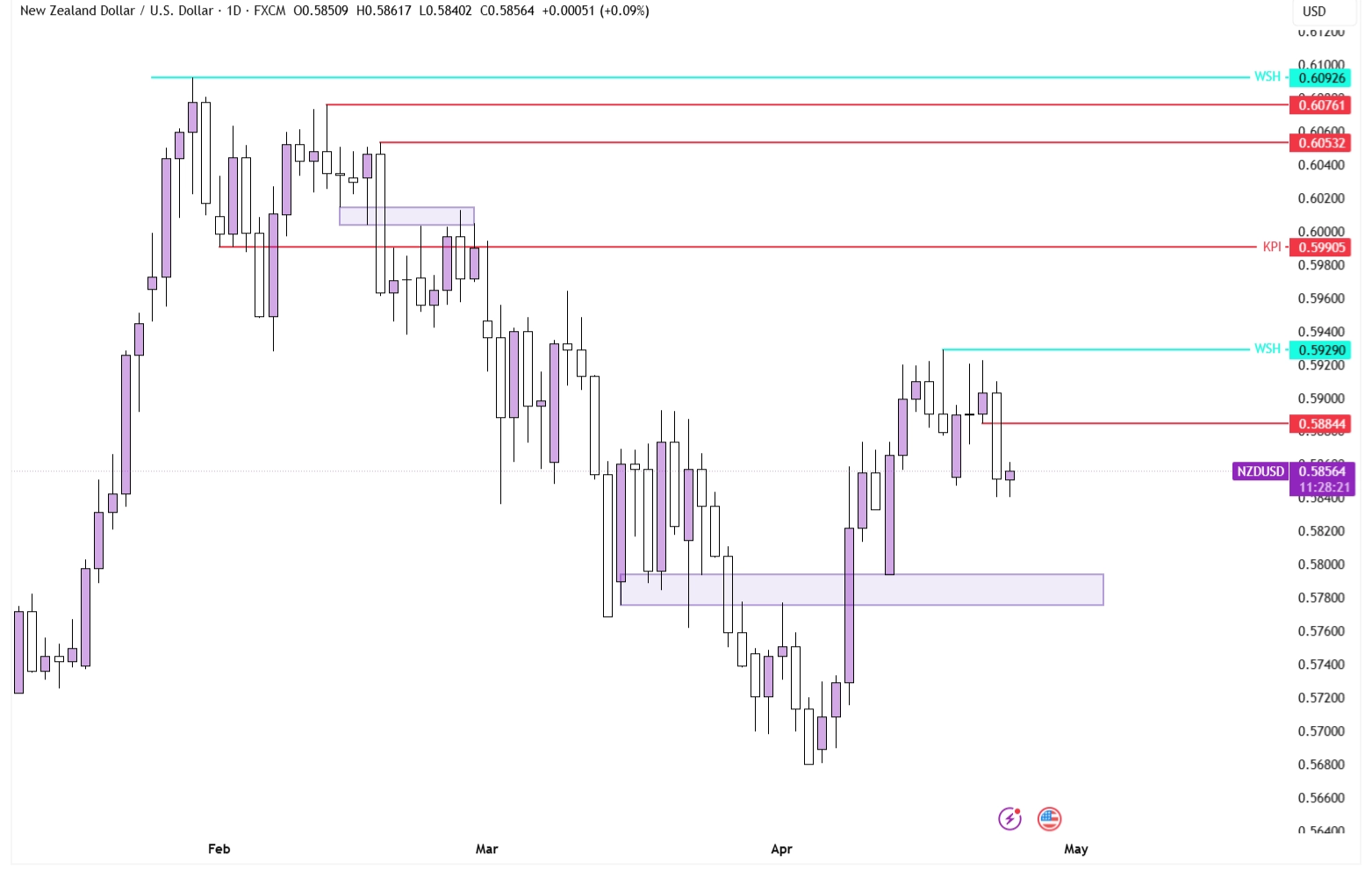

It was a calm week for the Dollar, as most pairs saw relatively little action.

NZD/USD on the Daily Timeframe

The New Zealand Dollar seems to slightly tip its hand in wanting to go down. After Thursday’s strong candle down, the price has been ranging at the bottom of that candle. The low of Wednesday’s candle, at 0.5884, is a key point of interest, from where price seems likely to react, especially if price does end up wanting to go down.

Commodities

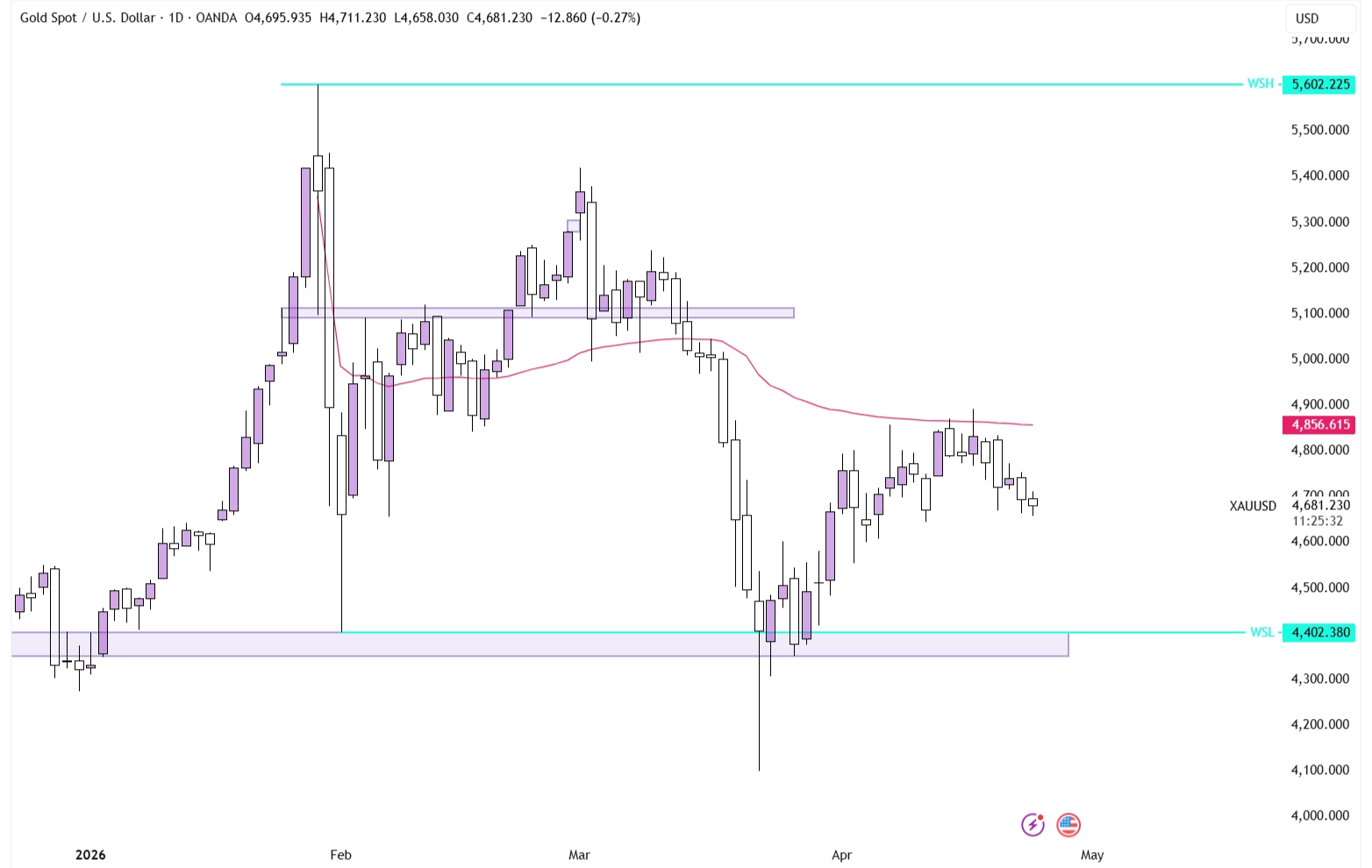

As Oil has calmed down for a bit, we’ll set our sights on Gold. After the January top, volume has drastically decreased, and price has retraced quite a bit from its prior highs, although the long-term bull run could still be intact.

Gold on the Daily Timeframe

As price got rejected by the VWAP anchored to the ATH, the picture looks slightly bearish on a technical side, although not overwhelmingly so. In the long run, the current consolidation might help to reignite interest in the market as buyers were exhausted over the earlier relentless uptrend.

However, what might be worrying for bulls is that Gold has been unable to rally materially on the back of the current geopolitical situation. Historically, Gold has always been seen as the prime geopolitical hedge, so the current lack of rising prices might hint that there’s more weakness in the market than the current prices indicate.

Conclusion

One-sentence summary of the week:

Markets across Stocks, Forex, and Commodities consolidate and brace for upcoming shocks.