Introduction

This week provided a relatively serene macroeconomic backdrop; however, the technical landscape across several asset classes remains remarkably active. Let’s dive into the details.

Global Macro

It was a particularly calm week in the global macro space. Australian CPI was this week’s sole high-impact event. Data landed at 3.8% YoY, slightly above the 3.7% forecast. This marginal overshoot keeps talks of future rate hikes intact.

With the calendar rather light, we’ll use this opportunity as a short reminder of where the three most important central banks stand policy-wise, and what to expect for the remainder of 2026.

- The Federal Reserve (U.S.): Interest rates remain elevated as inflation proves stickier than anticipated. Current consensus points to some lingering transitory tariff effects impacting the data. Markets are currently pricing the Fed Funds rate to settle in the 3.00% – 3.25% range by year-end.

- European Central Bank (ECB): Of the majors, the ECB currently faces the most straightforward path. With inflation hovering near the 2% target and the economy maintaining modest growth, the ECB is expected to keep rates stable throughout the year.

- Bank of Japan (BoJ): The era of ultra-easy policy is over, with rates now at 0.75%. The economic agenda of the Takaichi administration likely creates an inflationary tailwind. Interest rates are expected to be at 1.00 or 1.25% by year-end.

Equities

This week has seen further continuation of the earlier Japanese and European outperformance, as both the Euro Stoxx 50 and Nikkei made new ATHs, while the S&P 500 and Nasdaq spent more time ranging. Last week, we looked at the technical levels in the S&P 500, concluding that we were mostly in a ‘wait and see’ situation. That hasn’t changed yet.

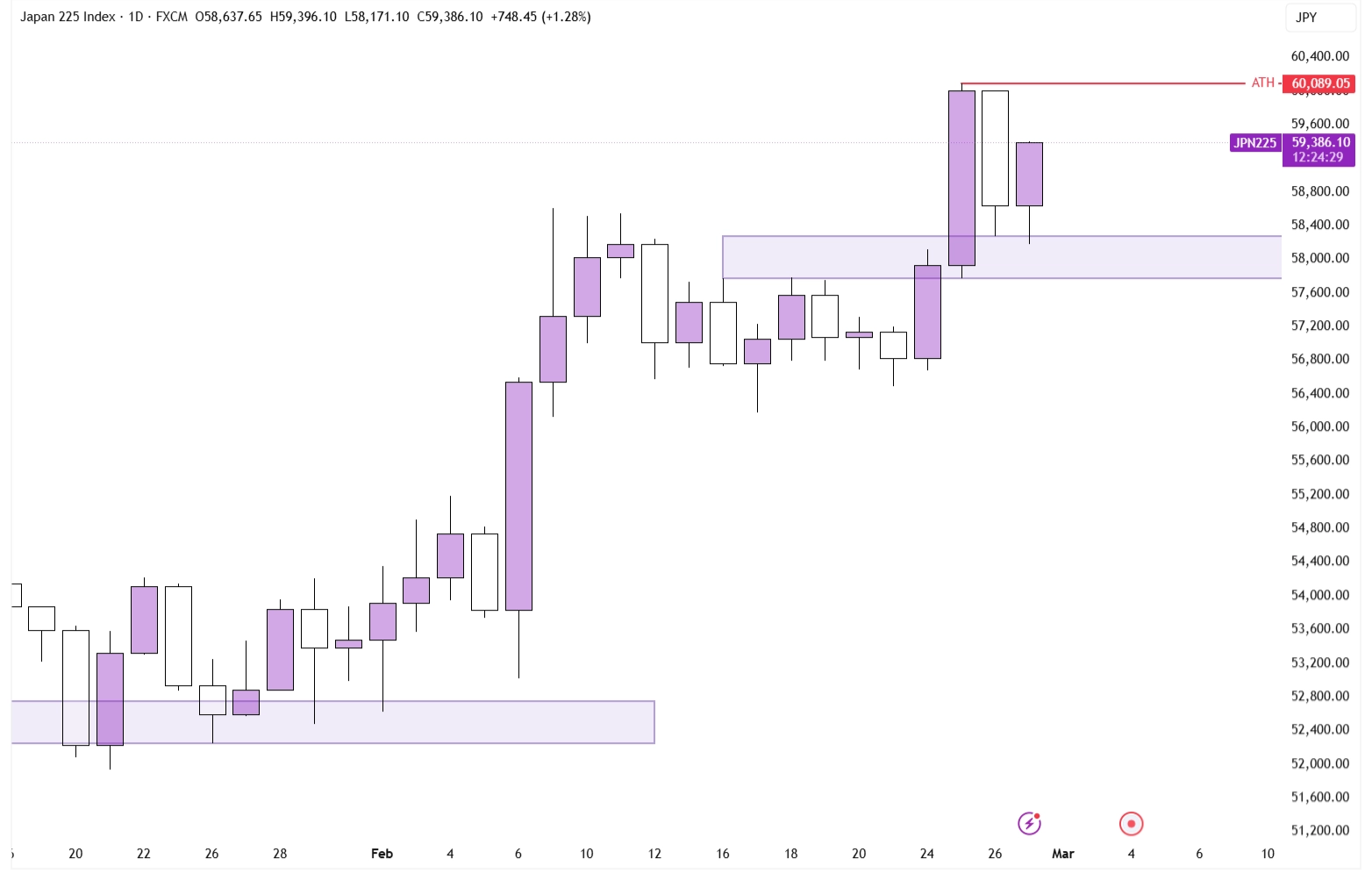

Nikkei on the Daily Timeframe

Instead, we’ll focus this week on the technical outlook of the Nikkei, which managed to hit the landmark ¥60,000 level this week. Because price has been in such a trending environment, the technical picture is rather straightforward:

Stay above the ¥57,700-58,300 range, and continued ATHs are very likely. On Friday, the price is doing just that, with the current candlestick potentially even set to complete a bullish engulfing, adding even more fuel to the current bullish backdrop.

As long as the long-term trend is up, it seems unnecessary to try to predict a top. Instead, it makes more sense to maintain a bullish bias, profiting from the momentum factor, where stocks/indices that recently went up are likely to continue going up.

Forex

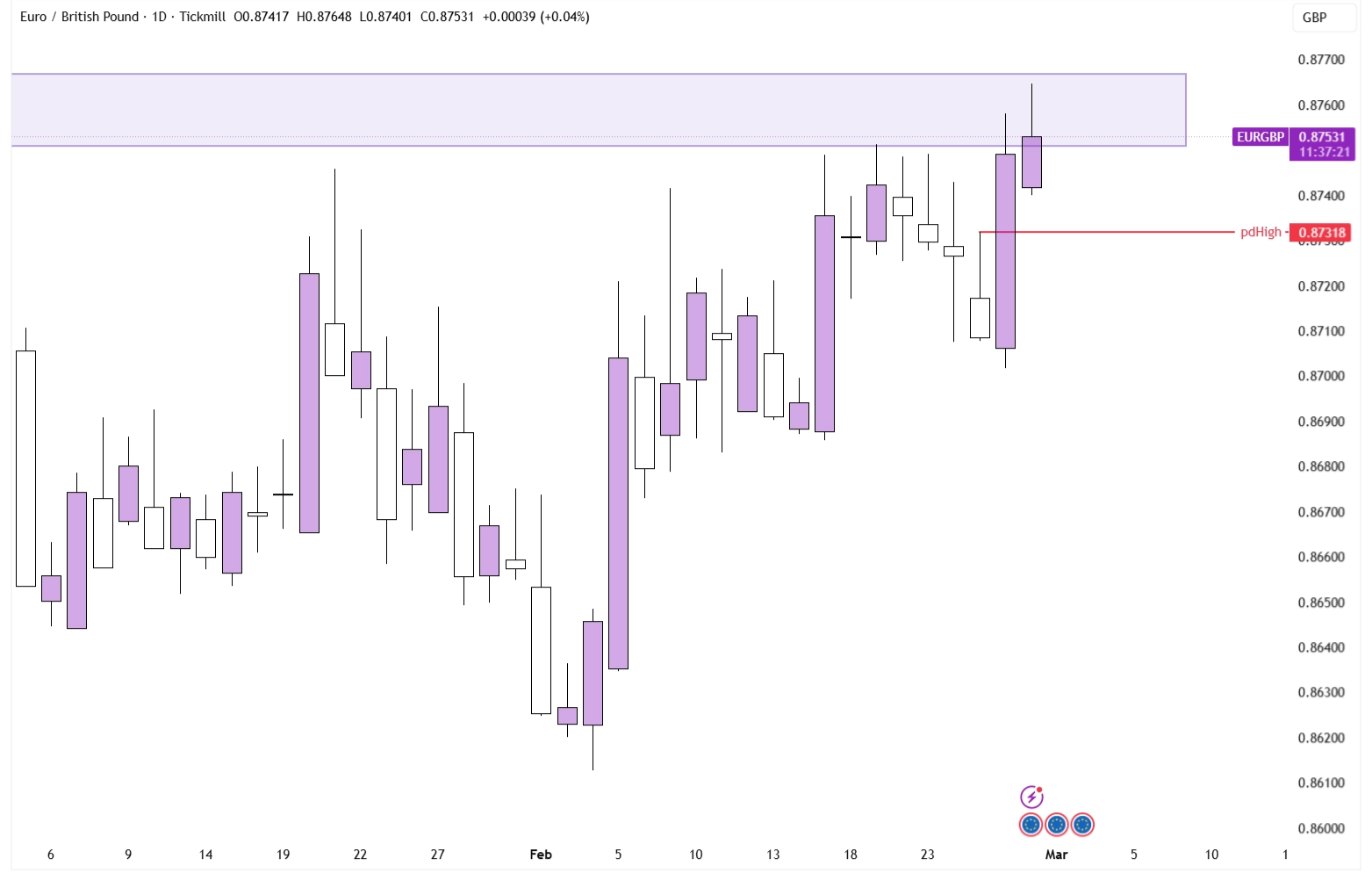

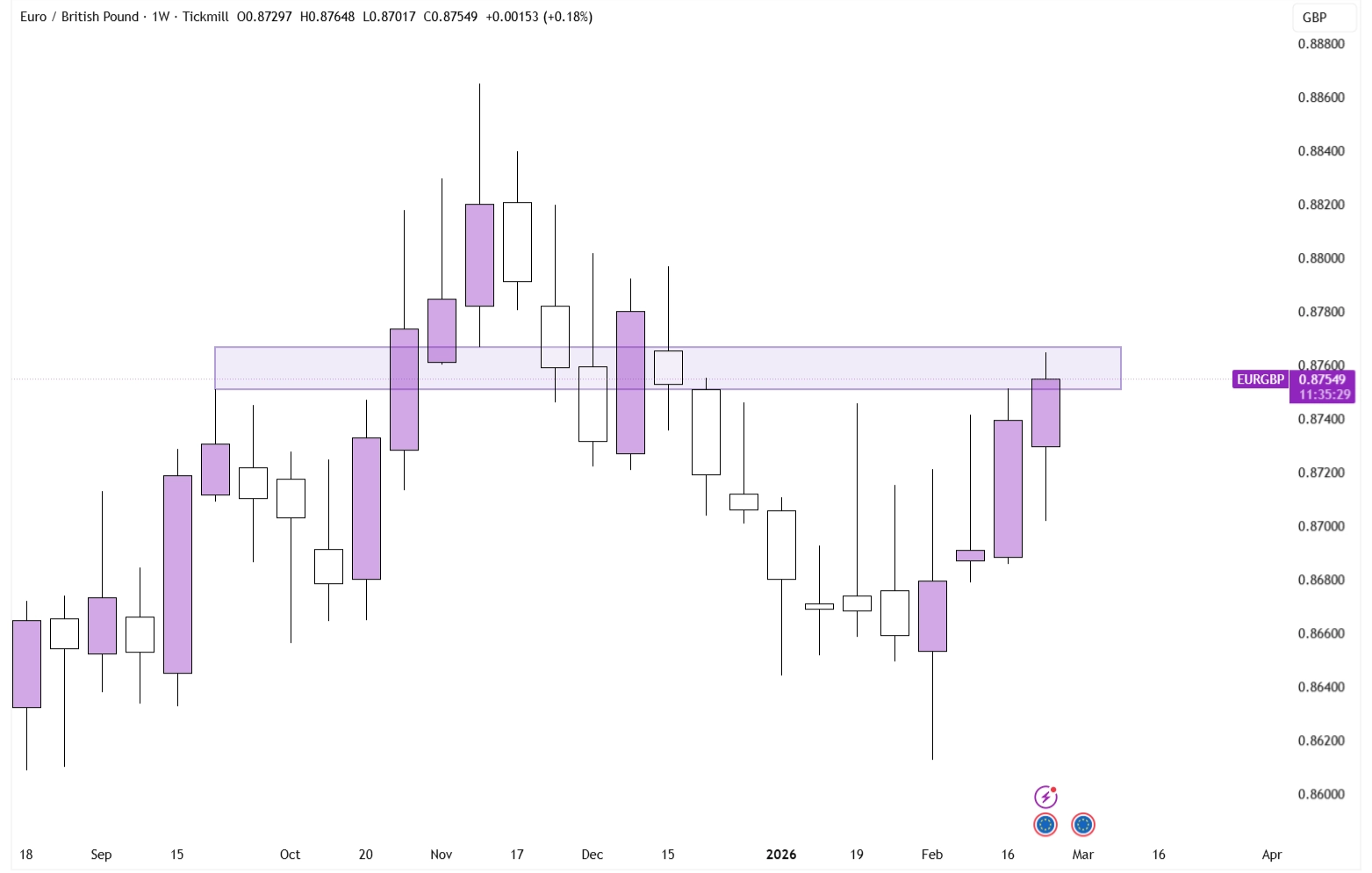

While the U.S. Dollar Index remained essentially flat this week, individual currency pairs offered plenty of movement. EUR/GBP, in particular, is creating a compelling technical structure.

EURGBP on the Daily Timeframe

On Thursday, price first took out Wednesday’s low, before then closing well above Wednesday’s high: the definition of a true bullish engulfing. Price is currently stuck between two strong regions. To the upside, we have a zone of resistance ranging from 0.875 to 0.8765.

EURGBP on the Daily Timeframe

To the downside, however, we have a crucial reaction point from the bullish engulfing. Traditionally, the high of the day before a bullish engulfing is an area where price is likely to turn from.

This leaves us with a possible trade idea, entering long on the support zone around Wednesday’s high, looking to target the zone of resistance above. When dropping down to a lower timeframe, we can visualise this idea more clearly:

EURGBP on the 1-hour Timeframe

Commodities

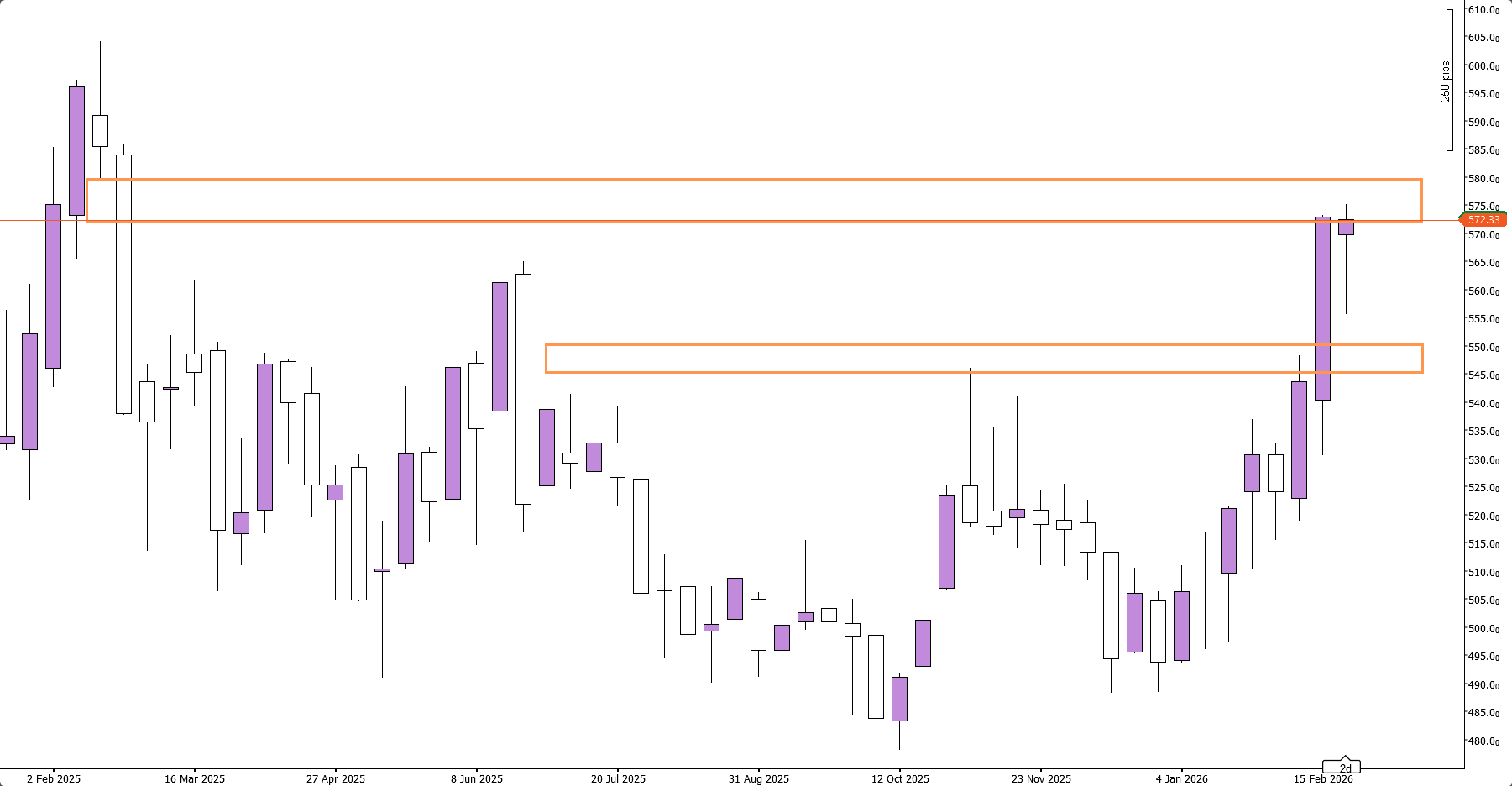

In the metals market, February was characterized by a staircase up grind: a slow, gradual recovery following the late-January correction. Wheat, on the other hand, had a stellar month.

Wheat on the Weekly Timeframe

Wheat has surged into a significant resistance area stemming from the 2025 highs, spanning $572–$580. A prime area for a short pullback is the supply zone of old highs, at $545-550, from where a continued move up would not be unlikely.

Conclusion

One-sentence summary of the week: Nikkei set for continued ATHs, EURGBP under pressure from both sides, and Wheat outperforming.