Introduction

For four months, the market has traded on a single variable: the war in Iran and the closure of the Strait of Hormuz. This week, that variable started to disappear. Washington and Tehran agreed on a framework to end the conflict, reopen the strait and lift the blockade on Iranian crude, and the deal takes effect today.

Global Macro

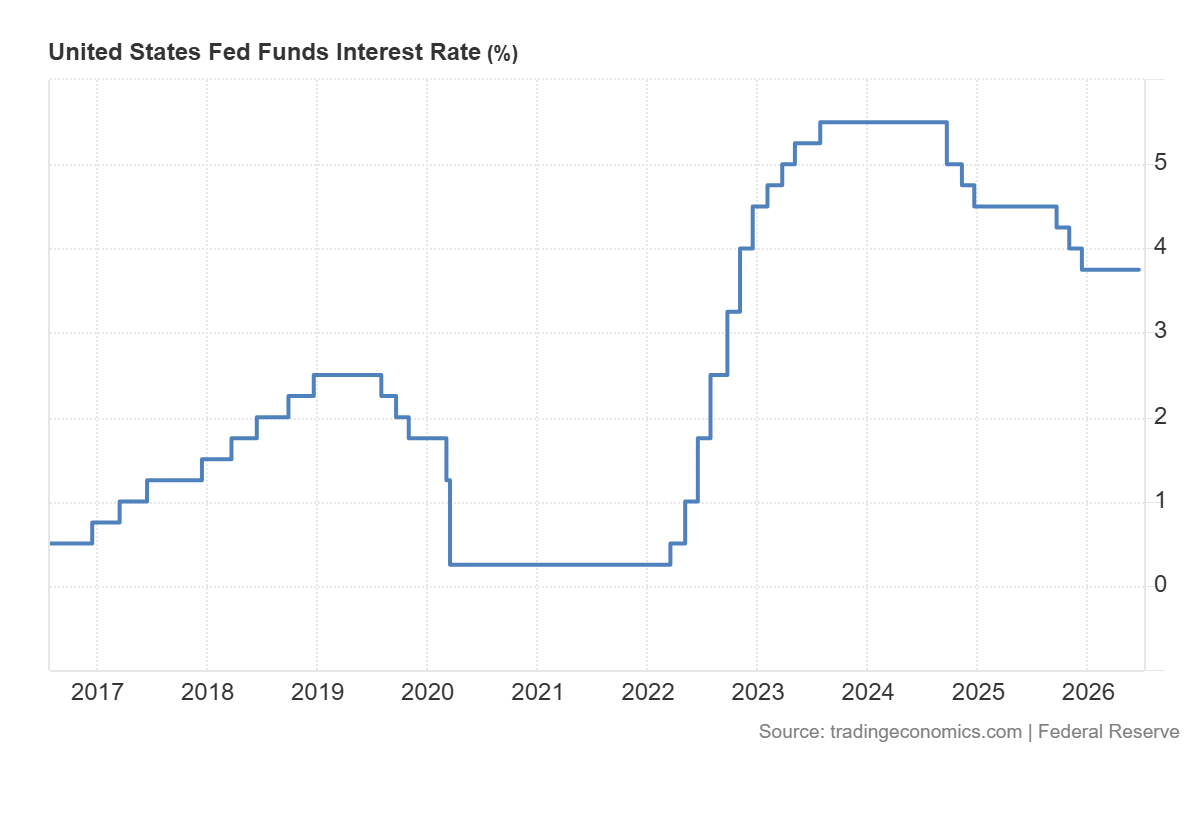

The Fed held rates at 3.75%, which was the broad consensus, but the speech is where things got interesting. On his first meeting as Fed chair, Warsh made it abundantly clear that inflation was becoming the priority again, and that the board was aware and unhappy about the fact that inflation had been above the 2% target for four years.

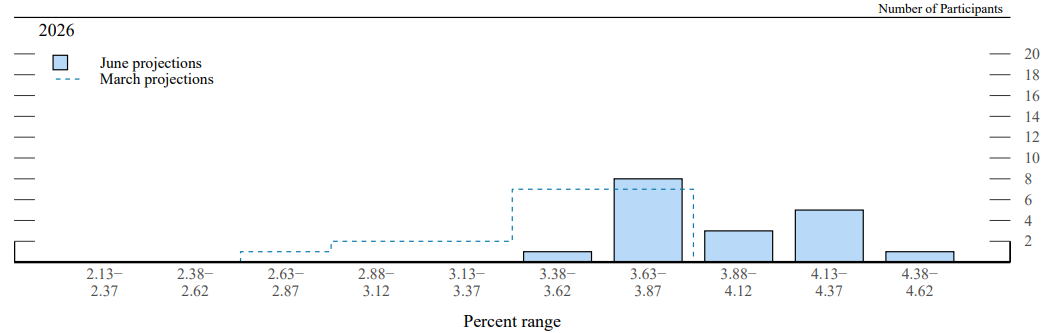

The meeting also gave us the infamous dotplot. The median dot for end-2026 moved up to 3.8% from 3.4%, with 9 of 18 members now expecting at least one hike this year. However, post-2026, they expect rates to drop again. This means that the expected rate hike is an insurance move, not the start of a new tightening cycle.

Expected Effective Interest Rate by End of Year, comparing March’s with June’s SEP Forecast

The catch is that these projections were built on a continuation of the war. With that geopolitical catalyst now out of the picture, the question of whether the Fed will "look through the data" reappears. The above chart, however, perfectly summarises the difference in expectations, now compared to three months ago, as the expectations are much higher. A final note worth considering is that Warsh himself refused to submit his dot, and there is thus one data point missing. Furthermore, he’s using the change of leadership as a good opportunity to review the current approach of the Fed, so changes to their approach should be expected soon.

Equities

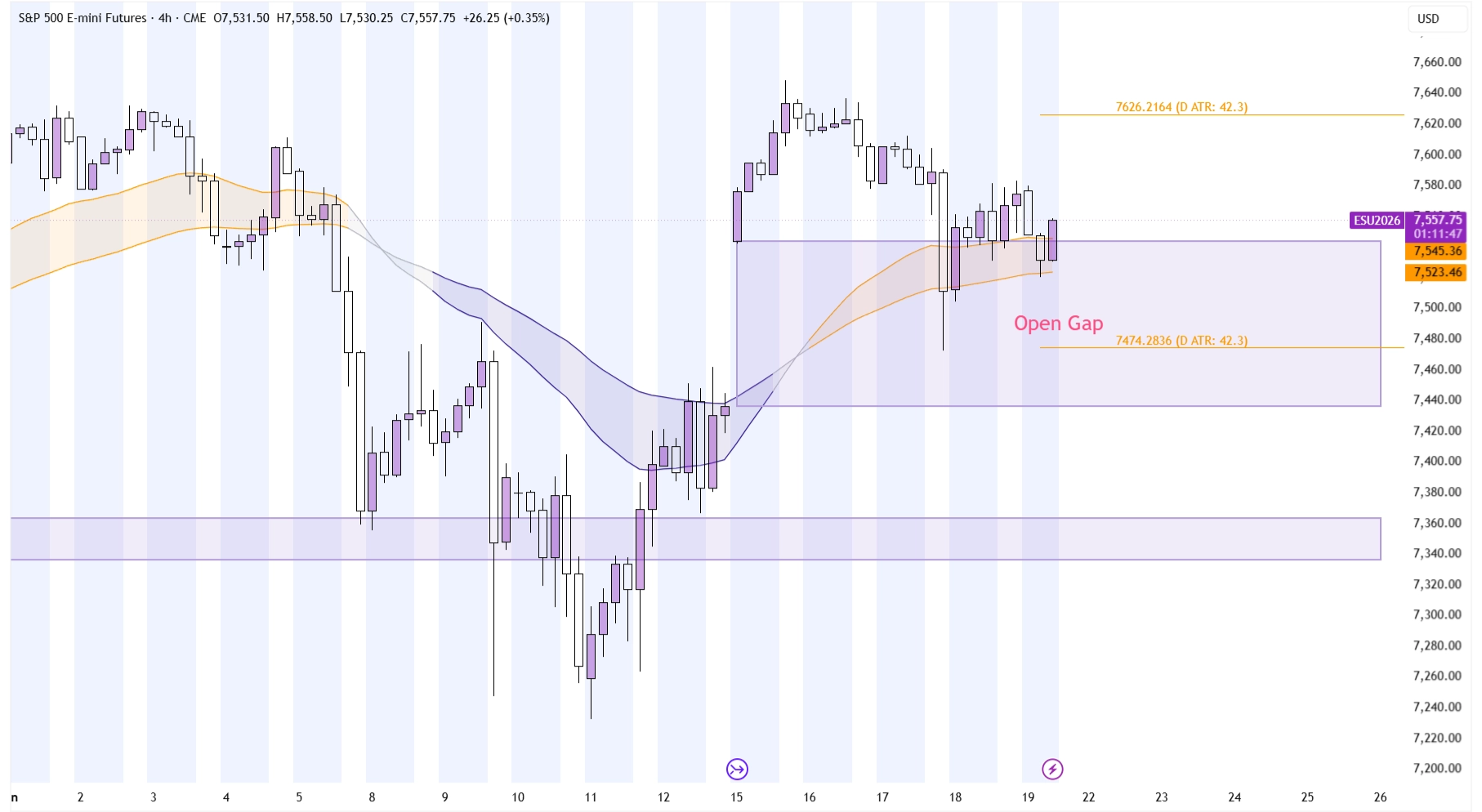

On Monday, the S&P as well as the Nasdaq gapped up on the news of the US - Iran conflict finally ending. Markets have continued to be able to hold that gap, despite the bearish news from the FOMC, as Warsh was more hawkish than expected, showcasing underlying strength in the indices.

S&P 500 on the 4-hour Timeframe

The fundamental picture couldn’t be more bullish. Even though Warsh was strict about inflation, the factor that was driving the inflation in the first place got taken out while the AI trade runs on. This does warrant the question, will the market do what’s most obvious (i.e. continue rallying), or was this a buy the rumour, sell the news event?

Forex

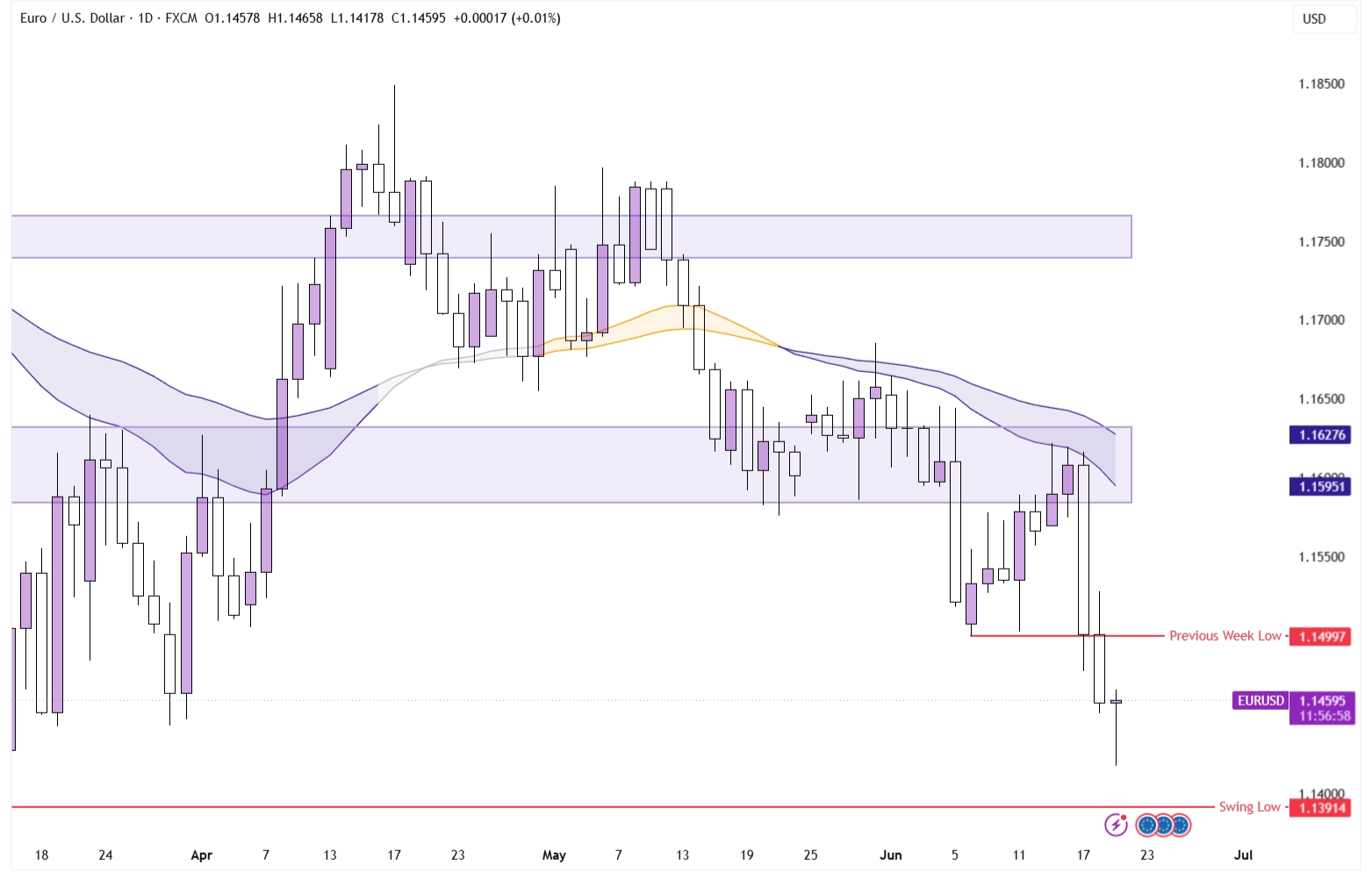

For the past three weeks, we’ve been focusing on EUR/USD, and for good reason. Despite an expected rate hike (which came to fruition) while the Fed was expected to hold rates, the pair was breaking down from a clear support area. This provided the opportunity of combining a failed breakout with a possibly dovish Warsh.

EUR/USD on the Daily Timeframe

However, that’s not what happened, as Wednesday’s FOMC prevented the reclaim of the support area and instead sent the Euro to new lows, as the weekly candle seems set to close as a bearish engulfing.

Because of this, the short-term trend indicates weakness, as the prior week's low at 1.15 becomes a key point of interest, and an old swing low at 1.1391 appears vulnerable.

Commodities

With the end of the conflict, how could we talk about anything but the conflict’s focal market of attention: Crude Oil?

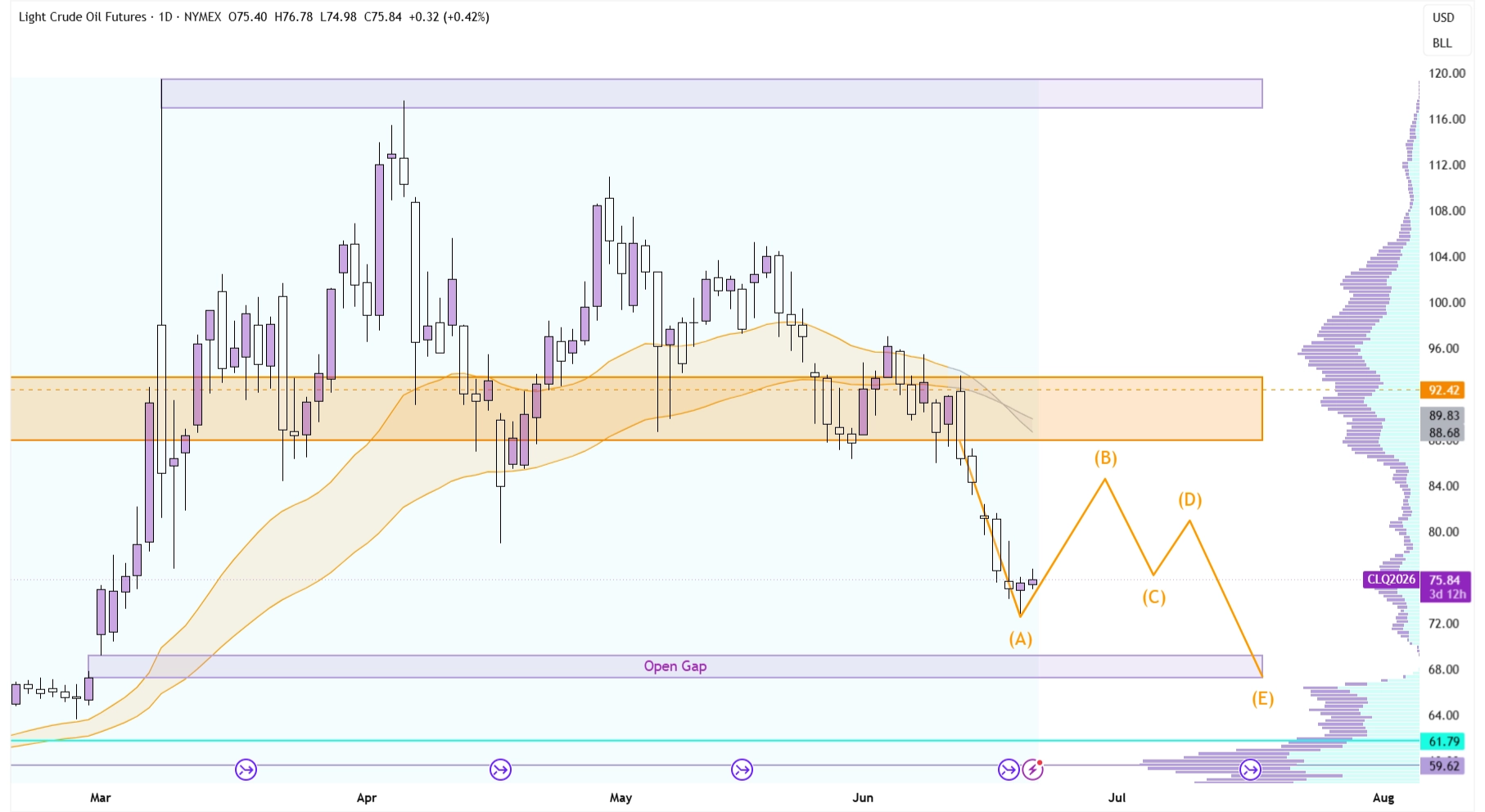

Oil on the Daily Timeframe

At the start of the war, the asset doubled in price over a timespan of just three weeks, and then promptly ranged for the remainder of the conflict. Now, as the situation has been resolved, the logical downside target seems to be the point where the conflict started, $67.29.

However, it seems entirely possible that the target is not hit until a couple of weeks later, as the situation needs some time for oil flows to restore and inventories to be built back up again. That warrants a price path akin to the scenario drawn above.

Conclusion

One-sentence summary of the week:

Warsh Refuses to be the Dove We Thought Him to be, and Oil Falters as Peace Returns in the Middle East